California Electricity Imports - Part 2: Deeper Insights

Thank you for the enthusiastic response and thoughtful questions following my previous article on California’s electricity imports. This follow-up addresses your inquiries with additional data, clearer visualizations, and deeper analysis of California’s electricity market dynamics.

Key Observation

California’s residential electricity rates, averaging roughly twice the national average, starkly contrast with the lower rates in neighboring states involved in electricity exchanges. This disparity underscores the unique economic pressures shaping California’s energy market.

Summary of Imports and Exports

On May 7, 2025, California’s electricity imports and exports, based on real-time pricing, revealed distinct market dynamics. The table below summarizes the data:

For May 7, 2025, California’s net imports totaled 39,598 MWh, calculated as the difference between imports (64,064 MWh at an average cost of $33/MWh) and exports (24,466 MWh at an average revenue of $5/MWh). This results in a weighted average cost of approximately $49/MWh for net imports. These figures are based on real-time pricing and are illustrative, as they do not account for specific power purchase agreements, day-ahead pricing, or locational marginal prices (LMPs). The data suggests California purchased electricity at a higher cost ($33/MWh) and sold excess electricity at a lower rate ($5/MWh), reflecting market dynamics on that day.

Analysis of Imports and Exports

To clarify the data presentation from my first article, I’ve separated imports (expenses) and exports (revenues) for easier interpretation. The graphs below, based on May 7, 2025, data, illustrate these flows.

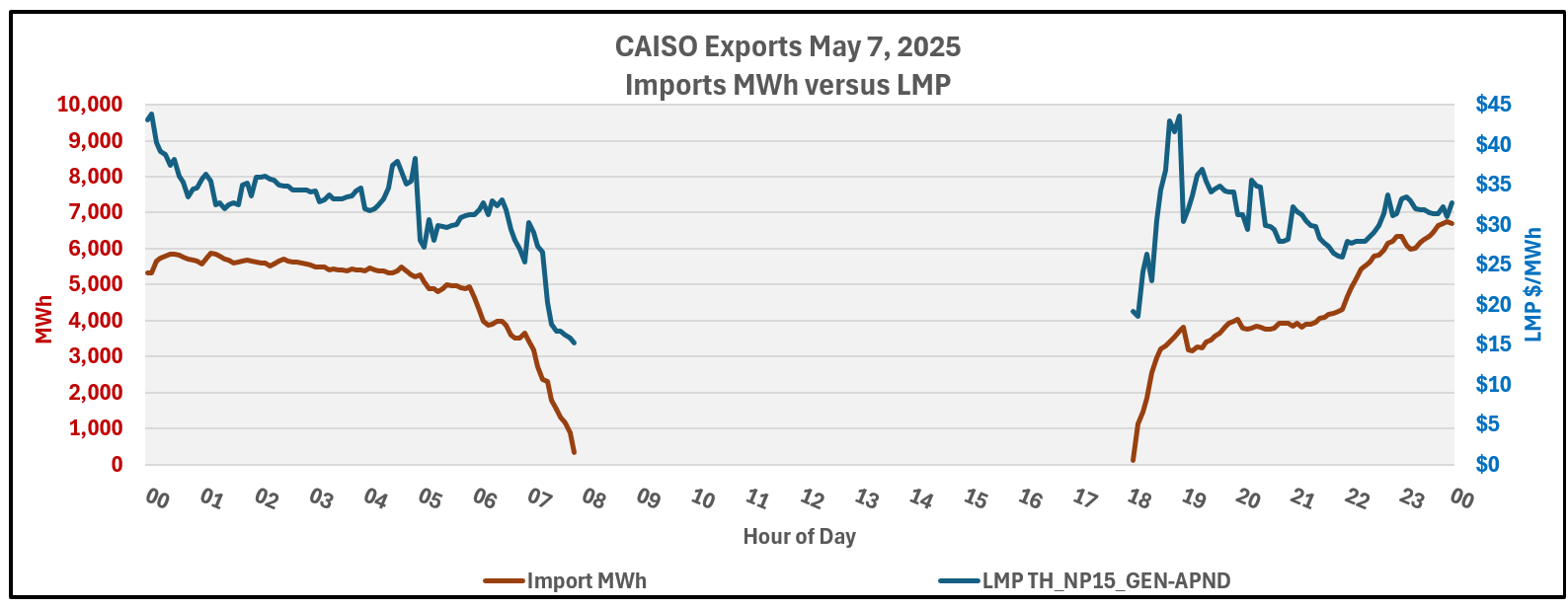

Imports

The graph below illustrates the volume of electricity imported (in MWh, shown in red) and the corresponding real-time pricing (in blue) on May 7, 2025. Prices ranged from $20 to $40 per MWh, with a weighted average of $33/MWh, representing the cost to import electricity from neighboring states.

Exports

The following graph shows electricity exports, primarily occurring between 8 AM and 6 PM, with real-time pricing ranging from -$20 to $40 per MWh and a weighted average of $5/MWh. This represents the revenue California earned from selling excess electricity to neighboring states.

Clarifications and Context

Net Imports: The term “net imports” as I am using it refers to the difference between total imports and exports (64,064 MWh - 24,466 MWh = 39,598 MWh). This metric is critical for understanding California’s reliance on external electricity sources.

Pricing Variability: Real-time pricing fluctuates due to supply, demand, and market conditions. Negative export prices or very low, if present, may indicate oversupply, where California pays other states to take excess electricity, often due to high renewable generation (e.g., solar during midday).

Limitations: The dollar values provided are simplified estimates based on real-time pricing for a single day. Actual costs and revenues depend on complex factors, including long-term contracts, day-ahead markets, and regional grid dynamics.

Your questions and feedback are welcome—please share them in the comments or via email.

Notes for Data Sources:

All MWh data is from the CAISO website.

The LMP data is from GridStatus.

The residential electricity rates for 2024 are from EIA.

Thank you Kerry for your clarifications regarding California's ongoing need to import electric power. California's electricity needs have persistently outstripped the state's ability (or desire) to generate power within the state. Think of Hoover Dam starting generation in 1936. Some of that power was exported to southern California. The Pacific DC Intertie which typically moves power from Washington state hydroelectric plants to southern California entered service in 1969. The 2,040 MW Four Corners (coal-fired) Power Plant operated from 1963 to 2023. Some of the Four Corners power was consumed in California. The 1,900 MW Intermountain (coal -fired) Power Plant near Delta, Utah continues to supply power to LADWP in southern California.

For several reasons, the export capacity of those out of state generators continues to diminish. The problem for California which was demonstrated during the ENRON crisis about a quarter of a century ago is California's demand for electricity is essentially inelastic, particularly as a consequence of business demand. Economic opportunists such as Warren Buffett apparently see this problem as a business opportunity to sell even more coal-fired power to California. That is what he is gearing up for with his support for California SB 540 (Becker, 2025) which is his latest iteration for CAISO grid regionalization after AB 813 (Holden, 2017) and AB 538 (Holden, 2023) were both properly rejected by the California legislature as harmful to the state's interests.